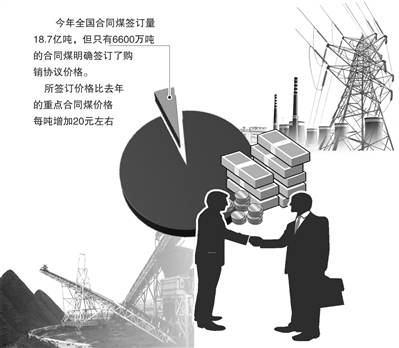

At the end of 2012, the relevant state departments seized the opportunity to gradually slow down the supply and demand situation of electric coal and basically stabilized the price of electric coal, issued relevant guidance, and proposed to cancel key contracts from January 1 this year and implement coal prices. The National Development and Reform Commission has also clearly stated that since January 1st, the temporary price intervention measures for coal power will be lifted, and the electricity coal will be negotiated by both parties. The stalemate coal coal prices have been breaking ice for years. However, from the first round of coal negotiations after the cancellation of the “dual track systemâ€, there are still differences between coal and electricity companies in terms of price, capacity allocation, transaction transparency, etc. The game surrounding coal prices continues. Each January is the month in which coal production and transportation needs to be negotiated and signed. In the context of coal prices, the development of coal production and transportation needs to be closely followed by the society. In mid-January, the China Coal Transportation and Marketing Association took the lead in organizing coal and power companies to convene coal production and demand linkage and assembly meetings. From the information reflected at the meeting, after the abolition of the "dual track system," coal and electricity companies still have differences in terms of price, capacity allocation, transaction transparency, and so on, and the game between each other has not been effectively resolved. The China Coal Industry Association has now completed a summary of coal production and demand linkage and signing. According to statistics, the national coal contract volume this year has increased by 55.8% from the previous year's 1.2 billion tons, setting a new high since the contract was held. Wang Zhanjun, chairman of the China Coal Transportation and Marketing Association, told the reporter that, strictly speaking, due to the adjustment of the statistical standards for coal contracts this year, the aggregate amount of 1.87 billion tons is not comparable to previous years. "However, this year, the supply and demand contracts have generally been compared. smooth". In this year's purchase and sales contracts, only 66 million tons of contract coal have clearly signed the purchase and sale agreement price in the contract, and the signed price has increased by about 20 yuan/ton compared with the price of the key contract coal last year. Li Chaolin, a marketing expert in the coal industry, told reporters that when the “dual track system†was implemented, it was difficult for buyers and sellers to reach a consensus in the coal market's expectations, and there were obvious differences in the price trend. After the price was consolidated, the decision-making power of coal prices was handed over to the market, and the uncertainty of price fluctuations increased significantly. Under this circumstance, adopting the approach of “signing the number of purchases and purchases by both parties and the price will follow the marketâ€, the coal and electricity companies are more likely to accept it. However, some experts have expressed concern about whether coal production and demand can be successfully implemented. From the previous year's situation, once the market price of coal has risen sharply, coal companies often use various means to disguise the supply of key contract coal in disguised form, resulting in the use of coal for power companies. Last year, due to the continued decline in coal prices in the market, the price of key coal contracts in some regions was inversely related to the market coal prices. Some power companies abandoned the key contract coal signed at the beginning of the year and purchased large quantities of coal in the market. After the coal price decision is handed over to the market, the coal price seems to be determined by the supply and demand situation, but on the whole, the coal industry’s bargaining power is more obvious. At this time, only by ensuring that the price formation mechanism is open and the market price is transparent, the contract can be performed smoothly. In addition, after coal prices merged, the National Development and Reform Commission will no longer issue an intentional framework for the inter-provincial coal railway transportation capacity allocation in the year. Due to the limited capacity of railways in China, it may affect the efficiency of resource allocation, and it will also become another “stumbling block†for coal market reforms. Experts suggest that the relevant departments should speed up the improvement of the coal transportation market, based on the contract and transport capacity signed by the coal supply and demand sides, rationally allocate capacity and maintain relative stability, and give priority to medium and long-term coal contracts signed by large and medium-sized coal-fired power companies. Coal companies say coal prices are not yet clear The price of thermal coal contracts has become a sensitive topic for Shanxi coal companies. Many coal companies take a wait-and-see attitude toward final pricing. At the same time, coal-fired electricity pools are becoming their new choice. Recently, reporters visited several coal companies and learned that in the 2013 coal price negotiations, many coal companies and power companies failed to agree on price issues. At present, many coal-fired long-term agreements have signed a "half-agreed contract" with no quantitative pricing. For a time, the price of coal contracts became a sensitive topic for coal companies in Shanxi. With regard to final pricing, many coal companies adopted a wait-and-see attitude. This situation has a lot to do with the stagnant state of the coal market since 2012. Moreover, after coal resources were consolidated in the past few years, many small coal mines in Shanxi were merged, restructured, and rebuilt. In the future, they will release more production capacity. “We have found that various companies seem to have such psychological preparations that the long-term coal power coal deal will be an annual contract, short-term pricing, and some even propose monthly and quarterly pricing. In fact, this is also in line with market rules.†China (Taiyuan) Coal Trading The deputy director of the center, Yu Shichun, said. It is worth noting that on December 27, 2012, the five major coal groups in Shanxi, Tongji Coal Group, Shanxi Coking Coal Group, Yangmei Coal Group, Shanxi Coal Group, Chun'an Group, etc., together with Yuze Power, Minshan Electric Power, Taiyuan No. 2 Power Plant, Linfen Power companies such as the Second Power Plant have successfully signed a coal and electricity joint venture agreement. Coal and electricity joint ventures are becoming new choices for coal companies and power companies in the market-oriented reform of electric coal. It is understood that at present, most of the 200,000 kilowatt-plus main generating units in Shanxi Province have coal and electricity joint ventures, and all have achieved profitability. The strategic alliance with equity as the link has enabled the coal and electricity parties to meet directly. On the one hand, the provincial coal mine coal mine association has signed it very quickly and on the other hand, it has also reduced intermediate links. According to the plan of Shanxi Province, by 2015, thermal power companies in Shanxi Province will all achieve the long-term cooperation contract management of coal, and some thermal power companies and coal companies will complete strategic alliances with equity as the link. Power companies say that power companies are optimistic about short-term pressure The introduction of coal price marketization may have some impact on the operation of some power companies, but overall, the current coal price level is a good time for reforms. After the introduction of coal-fired market reforms, what impact will it have on power companies? An electric power company executive who asked not to be named told reporters that in the past, the coal price was high, and the electricity coal included in the order range had a certain price difference with the market price, but the quantity could not meet the demand of the company. For the insufficiency, power companies also have to buy market coal. “This has advantages and disadvantages for power companies. Some companies that can get large orders can absorb the pressure of rising coal prices. But under the circumstances that the market price of coal and planned coal is very high, how can we ensure fair distribution?†he said . It is understood that coal accounts for more than half of China’s total coal consumption. In order to guarantee the supply of power coal, China has implemented government-guided prices and key contract management for coal that has been included in the scope of the order for a long time. However, in actual operation, it caused a certain degree of unfair competition, some disputes occurred during the signing of the contract, and the implementation of a low liquidation rate. He believes that the marketization of coal is the general trend. The introduction of some power companies may have a certain impact, but overall, as coal prices are now lower, the prices of planned coal and market coal are quite close to each other, and even there is a certain degree of inversion. This is a good time for the introduction of policies. The Guiding Opinions on Deepening the Market-oriented Reform of Thermal Power Coals proposes to continue to implement and continuously improve the linkage mechanism for coal and electricity prices. When the fluctuation rate of thermal coal prices exceeds 5%, the annual on-grid electricity price will be adjusted accordingly. The rate at which companies absorb coal price fluctuations is adjusted from 30% to 10%. The relevant person in charge of the State Electricity Regulatory Commission stated that this is very important. Otherwise, if the economic situation improves, there will be a substantial rebound in coal consumption in the future and the price will be difficult to adjust. In this case, the power companies will find it difficult to accept coal. The pressure of rising prices may even lead to policy-wide losses across the industry. The 0-10V dimmable series of Constant Voltage Class 2 LED Drivers from ZHPOWER offers both UL 8750 Listed and CLASS 2 rated. With universal input voltage ranging from 120VAC, the series of 12V/24V DC led drivers are designed for commercial, industrial and residential applications. Our 0-10V dimming delivers smooth flicker-free linear dimming down to 1% with most LED`s and a wide variety of compatible dimmers. Dimmable Led Driver,Ul Class 2 Dimmable Driver,Dimmable Led Driver 48W,Led Driver Dimmer 80W Shenzhenshi Zhenhuan Electronic Co Ltd , https://www.szzhpower.com